Regarding the (Collapsing) Banks

As usual, the Headlines won't tell you the truth.

(writing this very fast due to limited time today, excuse the result. Also my first use of substack rather than a very long thread. Let me know what you think).

As most anything threatening the financial house of cards, it is government mandated (as is the whole edifice). So we have to look at specifics of the mandates to have an educated guess of what may occur. The mainstream headlines of "greed", "excess" and "underregulation" are meaningless fodder.

(Never understood how all financial crises are based on "greed". Everyone was happy with the "greedy" people while they made lots of money. They are upset with them, when they lose everything. How did their greed encourage them to lose vast amounts if not of all of their wealth? Furthermore, the people that are upset with them, are upset at financial losses of their own... due to their own greed. It is odd for people that want more money and are upset at having less to accuse others who also wanted more and now have less that they are to blame for having wanted more (and instead lost). After somehow erasing greed, government regulation is touted as the answer. Never is the failure of the ever increasing government regulation criticized or analyzed (same with everything from a plane crashing to an oil spill)).

Back to our current situation. Share price of Banks in general and regional banks more specifically have been hammered lately due to a panic of bank runs. This started during the "failure" of SIVB & Signature Bank. The headlines mostly indicate that banks, such as First Republic bank, $FRC, are in trouble due to an ole fashioned bank run. Depositors are fleeing with their deposits. This people believe, will cause the bank to fail.

Though I will not delve deeply here into the financial plumbing that is our current house of cards system, leaving that for another day, I will try to summarize (& by necessity somewhat over simplify). Bank runs exist in the imagination due to the inherent "ponzi"-like nature we are led to believe that are banks.

We deposit money available on demand, say in a checking account, that we can withdraw at any time, and in reality the bank loaned it out for 30 years for a mortgage. So, as long as very few demand their balances, the bank thrives on, but if folks want to withdraw their cash, it is not there... it paid for other people's houses.... and the bunk fails in a bank run. This is not really the case. Not anymore and not really ever in quite that way. Today, banks really can manufacture money out of thin air... all they need is a credit-worthy borrower. They can only manufacture it by lending (they can't just make up money and credit it to themselves). They in fact inflate the money supply on top of Federal Reserve money. The money they create is indistinguishable from Federal Reserve Base money in the general economy. This by design of the very un-free-market system we have which is usually touted as the cornerstone of capitalism.

As people's demand for cash dwindles to zero (partly due to technological innovations and greatly due to government regulation. Today it seems like the government who physically prints currency also has banned it. Try to conduct any sizable business in cash today and you will experience this phenomena), cash reserves for banks became less and less important. In fact, today there are no real reserve requirements on banks. Nor do deposits limit banks ability to lend.

A bank will approve or decline a loan based on the credit & risk parameters of the loan and borrower. You won't see a banker say "Oh, we'd love to fund your loan, great applicant, we just happen to be low on inventory (money) right now, just give us a few days and see if we can get some more deposits and fund your loan".

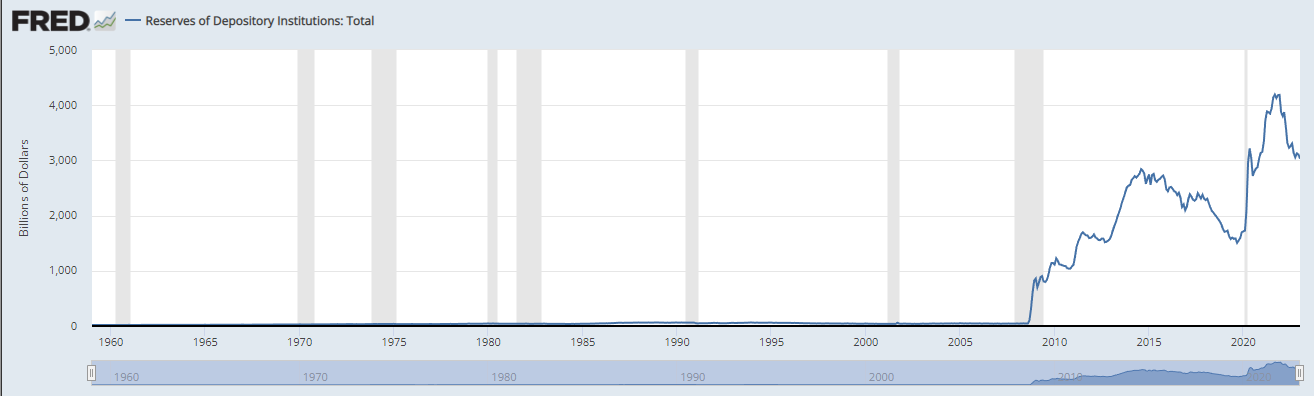

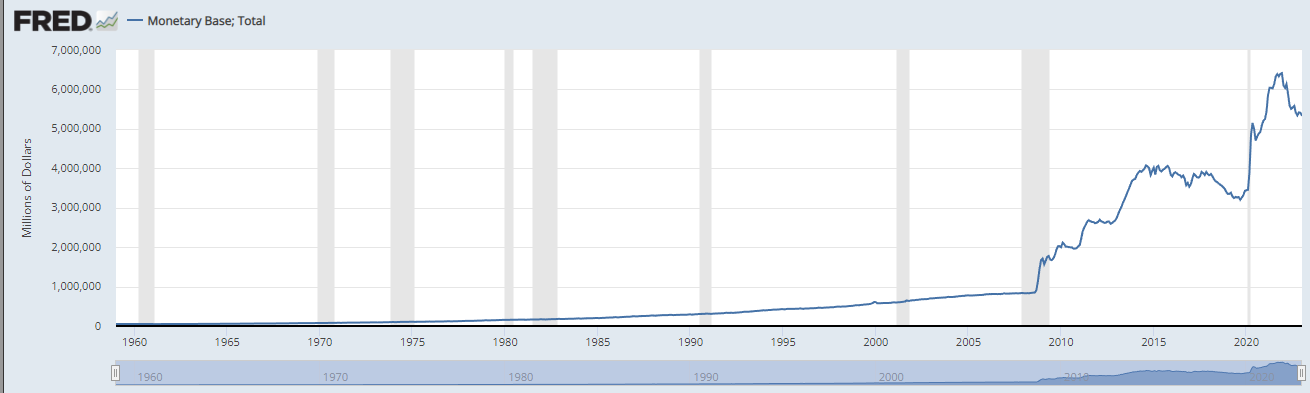

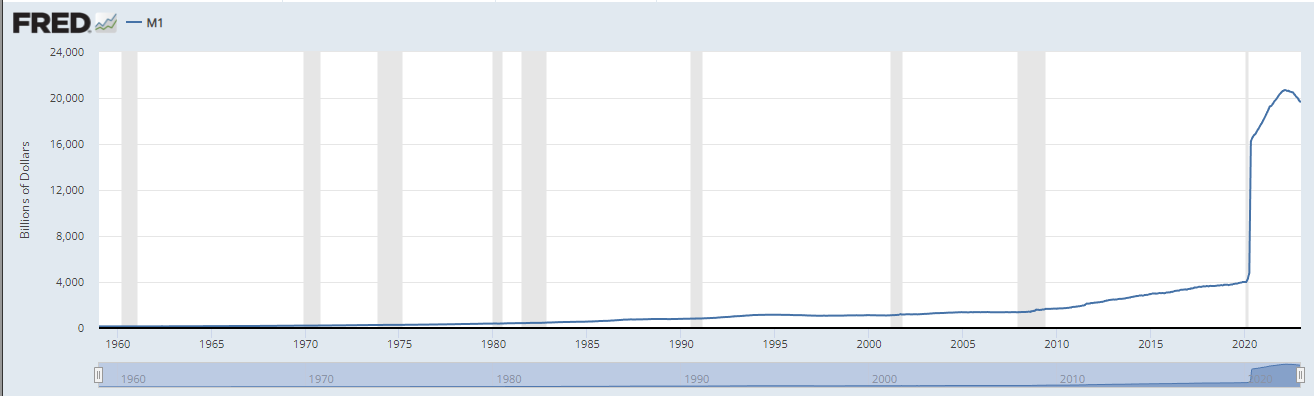

As cash disappears and the Fed's balance sheet exploded, bank's excess reserves are massive. As a whole, there is always plenty of money, and banks loan each other reserves on a daily basis virtually risk free. There are even large markets for deposits themselves in the form of CDs.

Note the fed's base money and the M1. Massive, inflationary explosion.

So today banks lend first and find liquidity later. When they do need liquidity, it is easy to find normally in the interbank market. When they can't, in times of turmoil and crisis, then the Fed's supposed (though often ignored) primary function comes into play. The Fed is the lender of last resort. It basically backstops the house of cards of short term deposits, and long term loans (plus the bank created money on top of it), by promising to create real base money in exchange for it at any time.

Traditionally this is by the discount window (though today there are quite a few different facilities with less stigma used much more frequently). The Fed will take bank's collateral, ie mortgage loans and mortgage backed securities, and lend newly created money against it. As much as any bank needs. This is why real bank runs do not exist anymore, at least not in the way we imagine them.

So if a solvent and sound bank, can get as much liquidity as it needs for its short term needs, then why do these banks fail? The government rules of course. The government sets up the rules of the game.

Just like in 2008, the main culprit for the "failed" institutions is the Fed (or other Federal or state agency that supervises that institution) seizes the institution. While banks are no longer limited by reserves, they are limited strictly observed capital requirements. The bank's capital (not deposits, which are liabilities to the bank and assets of their respective owners, but its own actual capital), limits the amount of (inflationary) loans it can give. The regulators are constantly measuring these parameters and are ready to seize a bank as soon as it falls below the required parameters.

These failures are rarely like those of any other business failing, namely bankruptcy. The bank does not hold up its hands and says well that's it, cant pay our bills, can't give our depositors their money to withdraw, game is over let's declare BK. Rather, one morning federal agents walk in and seize the bank, as they love to do (the actual agents I mean). The bank was not oblivious to this looming threat of course, and what was actually happening during their "troubled" time was them desperately fighting against abstract balance sheet parameters, and not going out of business in a classical sense.

A bank should go out of business if it gives a lot of bad loans which default. Or if its expenses are more than what it earns in net interest (after the defaults) in those loans. That is not what makes regulators seize banks.

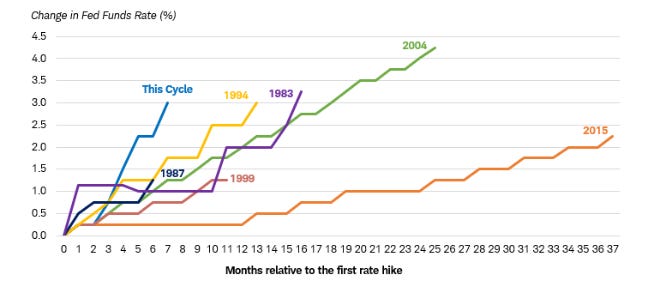

To make matters more ironic, its the Fed that created the fall in capital ratios which then justifies its seizures of the banks. The Fed has raised its rates faster and more steeply than ever before in modern history. It has done so to combat the inflationary monster it created (have a great previous paper on that, back when few believed their would be any inflation), by massive money printing.

When the interest rates go up, the market prices of banks' assets go down. Be they treasury bonds, corporate bonds, or mortgages... if the bank lent someone 100 dollars at 3% interest and now risk-free rates are 5%, no one will pay 100 dollars (par) for the same loan. They will pay ninety-something so that the yield they get it from it will be at current market rate and worthwhile. So the bank has a mark-to-market loss there, though it has not lost anything in actuality. If it does not sell the loan, then the borrower will ultimately pay the 100 dollars plus interest (and this happens most often sooner rather than later in a refinance or sale of the home).

Government rules however, require regulators to use mark-to-market accounting to measure the bank's capital (won't get into the complex rules here, including risk weighting, tier capital, and the handling of categories of assets held until maturity and those held for sale).

So in short, the Fed can create inflation, then raise rates sharply (when the the cycle is more moderate, banks have time to adjust their balance sheets and rollover capital to the new rates), making banks have huge losses on paper, and then seize them for it.

The flight of capital due to the fear of course is to the larger "too big to fail" banks, and so just like in 2008, the banking concentration gets worse rather than better, and the moral hazard increases.

All this being said (will like to come back to a more detailed piece on this later), what does it all mean for the current goingons. Well, firstly this was not meant to describe what happened with SIVB which had its own specifics and was CA state chartered, but what the situation is in general.

I thus contend that First Republic Bank $FRC, is unlikely to be seized by the government. This is because of the soundness of the bank, the Democratic party's freedom of movement across the federal bureaucracy (what is called "collusion" when done by Trump or the GOP), and the true nature of bank mechanics which I have described.

First Republic, does not need deposits to avoid the old fashioned bank run which no longer exists. The government is taking collateral at par and lending freely. The deposit issue is a concern for the longer term profitability of the bank. The deposits were a source of cheap to free source of liquidity for the bank. It can be replaced but for much higher rate moneys in the market (or the Fed). The bank needs to lend at the new market rates to continue to make money and hold on to the lower yield assets until maturity, early repayment (refinance / home sale), and/or lower rates set by the fed (which would once again raise their market value).

So the deposits and source of funds are an issue of profitability and long term survival, but not really a factor in the imminent regulatory risk. The Democratic party and the Biden administration desperately wants to avoid seizing more banks. So I believe $FRC may survive, be bought, offered additional backstops, but not be seized. Likewise other regional banks such as $WAL ($PACW though higher risk than WAL) and others.

This means the current share price is very attractive.

For lesser risk, there are the preferred shares such as FRC.K, PRC.H, PRC.I etc, and for the least risk its tradable bonds. The bonds are in my opinion a very safe bet (don't take my word for it, do your own research and invest what you can lose), and trading at half price.

Almost every scenario that may unfold would see the bonds being paid. They do require 250k minimum trade however, and the $WAL bonds require $100k minimum trade.

An anecdote to highlight how true it is that banks are shut down rather than fail:

In the 80's, a journalist asked the head Texas bank regulator how many institutions would go under the following year. After a moment's thought, he answered "156". The journalist was stunned by the precision of the prediction, but the regulator explained that the state only had enough auditors to close three banks per week. That is 156 a year.

The last bank closed the last week of the year could have been the first and vice versa. The bank fails when the government says it did.

I am betting, the Feds don't want to shut down $FRC, and so they won't. Let us see.

I also believe they will begin to signal that they are done raising rates shortly (but raise at least once more today, 25 bps, to not look like they erred & that they know what they are doing) since they will fear mounting bank collapses. The banks need more time to adjust their balance sheets and roll over rates.