Tariffs, Inflation and the Fed

The FOMC rate announcement upon us, and the Fed freezes in fear, and helplessness

We have discussed the Tariff issue with more detail in an earlier post, but a brief note on the subject is timely with the Fed announcement upon us.

The consensus, supported by Fed member’s own statements, is that they will hold rates steady and not “pre-emptively” lower them (though they may surprise everyone of course and end up doing it). The issue is that an increasing amount of data is showing that a drop would be wise, as the private sector is reeling from high rates (and the government spending cares not what rates are… prints money away, and simply pays the higher rates in a vicious cycle).

As always first a look at common knowledge (narrative as is much said today), gives us a good place to start. For our constantly misleading headlines, we can always turn to CBS and pals.

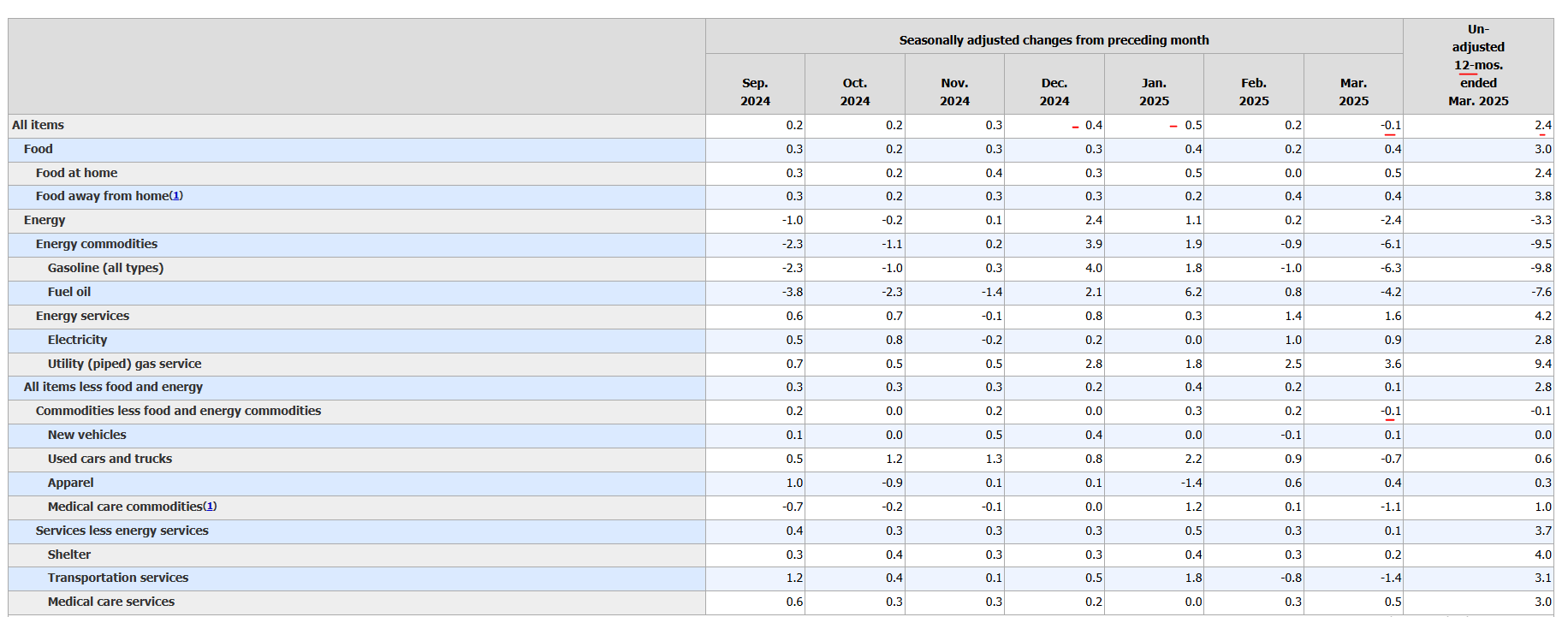

The media reported inflation at 2.4% in March, weather some reported it as “rose” like CBS or slightly “cooled” as some others. The truth is the report for March is of course, for March, and it was -0.1%. Negative inflation.

The “core” number (minus food and energy) was 0.1%, annualized at 1.2% (well below arbitrary target rate of 2%).

Interestingly, commodities other than food and energy (energy was a big negative of course) was also a negative at -0.1%.

In any event, the month’s release only tells us this new data point. And folks (and especially the Fed folks) are supposed to care where inflation is now, and where it will be (if they take no action, to then consider what action to take to influence that future rate); not where it has been (which they may have already taken actions to influence). To this end, the most recent month’s data is most important, though of course cannot alone be taken as a trend, as month data can vary significantly. A few months in one direction usually is good evidence of what is happening.

Therefore, the latest month is of most importance and the last few months are of key importance. Reporting the 12 month average, as the media does, is useless in a time of change (such as now). Everyone knows inflation had been high, which is why rates were raised. Constantly reporting the same months’ data nearly a year ago over and over is not actually reporting news, but reporting history as news.

Here are the recent numbers:

What ends up happening of course, is that the 12 month average is influenced just as much as the month being dropped (now 13 months ago) as the one being added. This adds a randomness and volatility to the headlines which obscure trends easily seen in the actual recent numbers. In periods where inflation was very high therefore, and rate increases have lowered it, you (the Fed) end up not waiting so much as to see that indeed the rate has dropped as much as simply waiting for the high rate months (or at least enough of them) to have now occurred more than 1 year ago and thus no longer influencing the 12 month average widely reported.

The CPI data itself is significantly lagged (note the latest we have is for March and we will soon to be in mid may before any new data is released), and then a much larger lag is introduced by looking at the last 12 month data (as opposed to annualizing the current or recent rates). This is one of the reasons why the Fed is consistently late.

Looking at our friends over at CNN for some misinformation, note that the headline does indicate inflation “cooling” in March (though in fact it was a negative inflation, so not cooled but non-existent and in fact reversed), but quickly warns us of the doom to come by (Trump) tariffs.

We have the image of the consumer facing empty (for US standards!) shelves for good measure. If we read on, we see that the 2.4% rate is not only reported, but importantly as a drop from 2.8% in February, a completely meaningless statistic. Obviously the impression it gives any reader is that the (annualized) inflation rate in Feb was 2.8% (though it was 2.4%), and in March was 2.4% though it was -0.12%!.

Reading on, we see no mention of the actual negative March number (let alone any further detail or analysis of it in detail).

Furthermore, the difference between the Feb and the March numbers, which are massive (a 150% reduction), from a number that was basically on target (2.4% in Feb) to a deflationary one, is masked as a much smaller change from 2.8 to 2.4 percent. And even this magnitude of a change reported was lucky, since the month that March’s negative data point replaced, was the previous March’s (2024) 0.4 percent, increasing the effect on the 12 month figure. If by chance it had replaced a month with a lower rate, its effect (in the reporting) would have been much lessened (if not reversed as often happens).

Similarly, the next month’s data will be replacing April 2024 which was also quite high at 0.3 percent, and will indicate a similarly reported drop. The Fed will look foolish by then; not having dropped rates.

Inflationary Tariffs?

Twelve month aggregations aside, clearly CNN’s reporting is mostly about the impending inflationary doom inbound, courtesy of Trump’s tariffs.

Again, we have discussed the tariffs elsewhere in more detail, but here we want to address this persistence reporting. Tariffs are not inflationary! That does not mean they are good or bad (all taxes are bad), but simply that they do not print money. Inflation is not the change of price of certain goods relative to to others, it is the rate at which the national currency diminishes in value. It is always understated because productivity increases and real price drops, mask its magnitude. This is what inflation really means or ought to mean as commonly used (or rather misused) but it is certainly what it means from the perspective of the Fed.

The Fed controls the price of money (interest rates) and the money supply. It has or should have no interest in specific price changes due to millions of variables (ie a new Ag-tech drops the price of food, but increases the demand on transport (importing more fertilizer and exporting more food for example), and raises the price of oil (& its dependencies) and travel). It should take fiscal policy into account, only in regards to its deficit spending which triggers an increase in money supply as the Fed monetizes the government’s debt.

Most importantly, even if considering the effect of tariffs as inflation (as all price changes in the defined basket of goods & services, regardless of cause are reported in the CPI), they do not constitute a “rate”. The reason these month over month numbers in the CPI are important is because they indicate a velocity, or rate of increase. The price changes overall invariably increases as the government prints more money. The value of the dollar keeps decreasing. It is not a particular month’s tiny .2 or .3 percent change that is the issue, but that it indicates a rate of change that continues… which is why it is annualized.

Inflation is ongoing and thus debilitating. The relatively low 0.2% month over month change, which is only slightly above target at 2.4% annualized, translates into a a 21.27% loss of value in 10 years. Your 100 dollars are now only worth $78.73, and in 20 years only $61.92!

The Fed’s Thinking

So what is happening here? Well, as tariffs start to be implemented broadly (if they ultimately are), they may increase the price of a significant number of goods and services in the CPI basket. When we are speaking of changes of a tenth of a percent in any direction being large variations in your typical CPI report, imagine what that may mean when compared to a sudden change in thousands of goods by much more significant percentages such as 10, 20, 40 and more percent?!

The tariffs effect on prices is yet to be determined because of many unknowns, most importantly what tariffs will in fact end up applied where as negotiations continue. Additionally, the resilient and versatile US economy will shift and maneuver to avoid a significant part of the increases (as an overly simplified example, if a country now is facing a 40% tariff for a widely imported good, and domestic production cost of it was only 15% higher than the pre-tariff price, than no one should expect to see a 40% increase in the price of the good, since it will be acquired domestically).

However, depending on how they are ultimately implemented, they may in fact cause one-time measurable increases in many goods and services. These changes have the potential to completely overwhelm CPI reporting in the short term (a few months of data). If reported as annualized rates (for a change), they could indicate unfathomable inflation. All it takes is for a CPI month over month to show a 5% increase in prices across the board (due to high tariffs implemented across the board), to be reported as a 5 x 12 = 60% inflation rate!

The meek folks at the Fed know this.

They are in no way afraid of tariffs as a source of inflation because as explained, they are one-time price change events, and in fact potentially reversible in longer term. As alternative suppliers are found (in non or less tariffed countries) and/or domestic production increases together much of the price change can be reversed over time. Not only are alternative suppliers found, but so are alternative goods. This is without even taking into account the negotiations that can lead to the lessening or removal of certain tariffs over time. Finally, consumption choices change with prices, so even though certain goods and services are in the CPI basket, it doesn’t mean Americans consume them at those rates regardless of the price.

It doesn’t matter that the price of a specific imported good went up 100x, if the result is simply that no one will then buy it. The economic acrobatics that would take place are impossible to calculate, and guided by Adam Smith’s invisible hand, will rebalance the economy accordingly to minimize the cost to consumers.

So if the Fed knows all of this, why are they so intimidated by the tariff inflation problem? Why do they want to wait until after seeing its effects to drop rates? Simple enough. We just discussed how one or more monthly CPI reports can contain unprecedently large price increases.. stuff the media will run with in glee. What would the Fed chairman explain at this point? That this is “transitory”? He won’t do that again you can be sure!

The Fed chairman, having been mocked by calling price increases fueled by inflationary money printing (by very few if any others, without hindsight as I happily did), will now call one-time tariff price increases inflationary (and thus non transitory) in fear of being mocked again. Therefore, the Fed is loath to drop rates ahead of CPI reports that may report unrelated (to inflation) price increases. So much for the independence and wisdom of the Fed.

The result? The Fed will be even tardier than usual in dropping rates to avoid a recession caused by their sharp and sustained rate increases. Meanwhile they remain powerless to curtail the actual cause of inflation, the endless and ever increasing monster of government spending (which cares not for the interest rate) and the corresponding deficit. This, as I hope to discuss with you further in another piece, remains the US’ most imminent threat (demographics aside) and the most important and historic problem the Trump administration is tasked with tackling1.

What to do?

For us, it at least may mean further opportunities in the market as people incorrectly (over)react to the media hype. We already did very nicely purchasing certain securities (should I publish the list we used?) at the tariff doomsday crash, already well along the road to recovery. Any unusually high CPI report if and after tariffs haven taken hold will probably cause all sorts of havoc to be enjoyed.

I hope the Trump administration successfully focuses on that task, which is a very challenging one indeed as we have discussed elsewhere, rather than the inevitable attacks on the Fed for not lowering rates along with the threats of firing the chairman. If folks are interested, I can discuss the legality of that, but it is sufficed to say that while replacing a Fed Chairman is a potentially beneficial action, threatening publicly to do is not. Given the number of fights the administration faces in all directions, it is one I would not take, and thus not bluff to take. Mr. Trump unfortunately, for all the great potential his administration holds, does not mind bluffing, and frequently. It is a technique (issues of honor aside) that perhaps worked better in private meetings as a businessman when all the counterparty knew about you is your wealth and fame. In politics and diplomacy, especially after you are well known, it works much less if at all, as people learn your style, and inevitably to increasingly call your bluffs. It is much better to pick the fights you are willing to win, and do so.